Time for GPs to re-evaluate their operational value creation models?

Tarang Kumar. 21 November 2022. On behalf of AccelNorth Partners.

It’s now coming up to a year since a number of the major world indices started to roll off their peaks, and we’re still somewhere between 15% and 30% off those peaks in many developed markets. What had been clear since the start is that this was likely to be a U-shaped recovery. What was less clear is whether this was going to be a |_| shape or a |______| shape. It is now clear that it is the latter, but there is no visibility as to when the U will start shaping upwards again.

Most simplistically, private equity firms have three levers of value accretion at their disposal — multiple arbitrage, EBITDA growth and deleveraging. For most GPs, if they are truly marking to market, their portfolio company valuations should have declined between 15% and 30% over the last 3 quarters on a pure multiple arbitrage basis. If the portfolio companies have the added ‘disadvantage’ of sitting in Europe or the UK, there’s also the c. 10–25% currency devaluation (translation effect) that EBITDA growth needs to make up for (even if you have a € or £ fund, your $ LPs are still going to feel that impact, regardless of what currency you report in). That’s a LOT of pressure on fundamentally growing businesses at a time when governments like the US and UK are pushing forward policies to slow down business and consumer spending.

With increasing interest rates, private equity businesses may pay back debt quicker than they would have otherwise, but (a) that driver of value creation is limited, by definition, and (b) excess cash used to pay back debt rather than reinvesting in the business has ramifications for the future growth of the business.

Therefore, private equity and venture capital funds (the latter to manage cash burn at a time when late-stage fundraising has becoming significantly harder), must focus at this point, more so than they have had to in the last decade, on driving core EBITDA growth.

A number of GPs will no doubt argue that they have been doing that anyway for a number of years. However, the real questions are (a) is the operational engagement model of the GP both well-defined and repeatable? (b) is it fit for purpose for the ‘new’ volatile operating environment?

Both public and private market investors have long commented that CEOs who are good for business growth are seldom the same folks who are good to also navigate trickier waters. Many consulting firms have separate divisions for restructuring and operational consulting vs growth consulting — for a reason. It seems natural to conclude that the same operating model that GPs used to engage with portfolio companies in bull markets may come under pressure in these ‘new’ but here to stay volatile markets.

We have been telling our clients for some time now to:

(a) define what value creation levers have worked for them in the past (especially through challenging times), and

(b) consider the portfolio company engagement model which is likely to work most effectively for their region, culture, ownership approach, typical ownership stake, etc.

Let’s consider each of these pieces in turn.

Defining a repeatable set of value creation levers which work well for you

In defining a set of value creation levers, a PE house must do some work to figure out what has worked for them in the past, ideally through the post-Lehmans downturn, and also what has worked more recently that is likely to work through the current choppier times. The work takes a mix of strong quantitative analysis built around attribution of success factors, as well as more qualitative analysis in interviewing deal teams and current portfolio companies.

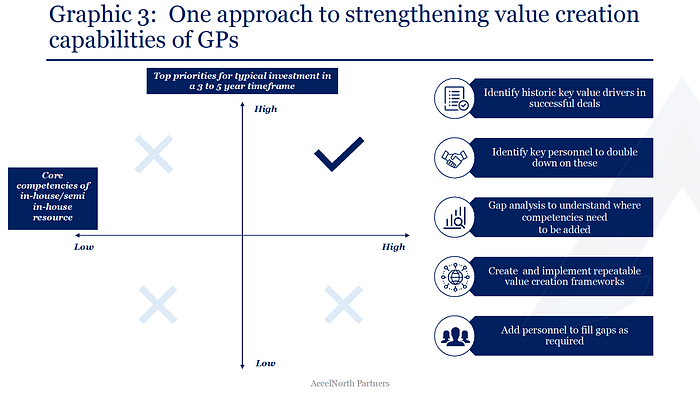

One example of some analysis we did for one of our European mid-market PE clients resulted in a framework which looked a bit like this:

Each PE house will have its own set of levers which work for them, and it is important to know which these are, and how relevant they are in the current environment. Do some of these levers need to be redefined? Is there requirement for personnel additions, or re-skilling?

Defining a portfolio company engagement model which works well for you

Over the years, the ‘big’ private equity houses have worked hard to trial and improve operating engagement models with portfolio companies which work well for them. In the early to mid-2010s, I saw LPs put pressure on mid-market and small cap GPs to also adopt similar models — generally to outcomes which were often unsuccessful; this was well-documented at the time, for example in Bain’s 2016 Global Private Equity report.

As an LP at the time, one of my observations was that these models generally struggled because a number of small and mid-cap GPs had started adding operating resource purely to please LPs — often a 1–3 member team, which did not have the same level of thinking-through that the big GPs had done at the time, nor did they have real belief and backing from the top of the house. Behind closed doors, some smaller GPs even admitted that they had added operating resource to please LPs (a bit like ESG resource at some GPs these days) but did not think that that resource added value, and actually often hindered the current modus operandi at those GPs. Little surprise then that those models didn’t add as much value as hoped (note, ‘hoped’ not ‘expected’).

As we once again go through volatile waters, the questions come up yet again — is the portfolio company engagement model well-defined and is it fit for purpose for the current volatile times? This question is relevant not just for smaller GPs, but also for larger GPs who have not had to re-evaluate their operating value creation model through the bull market (rising tides… all boats… yadiya) — and it’s time for them to do so again.

This summer, we were asked by one of the 5 largest GPs in the world to present to them different portfolio company engagement models which had worked for GPs around the world, as they re-evaluated what was and wasn’t likely to work for them through the coming years. Having considered a vast array of operating models, we honed in on 7 models, which we thought were sufficiently different and had worked well for the GPs in concern. We considered these 7 models to be sufficiently different and generally well-oiled, and were famously used by the following sets of GPs: Advent/CD&R/EQT, Apax/Permira, Bain Capital, Bregal Unternehmerkapital, Bridgepoint, KKR and TDR/Towerbrook/Triton.

Once a GP has sufficiently evaluated which operating model is likely to work for it in the years to come, it should then conduct a gap analysis to figure where competencies need to be added, begin implementing the frameworks at portfolio companies, and then iterate to get as close to perfection as possible.

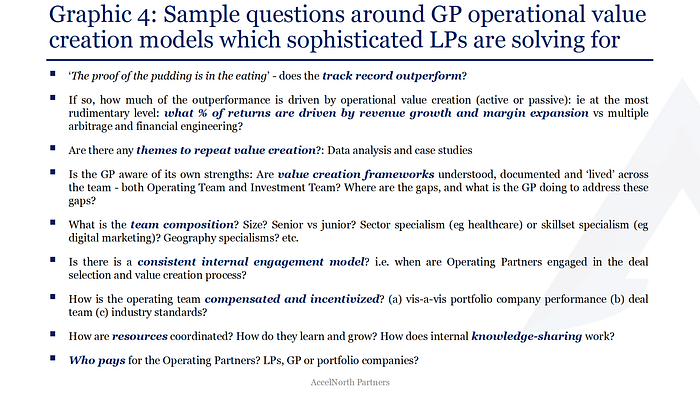

Lastly, as we always tell the GPs we work with, it’s not just OK to have great competencies, processes and frameworks in place, you need to be able to articulate these clearly and succinctly, and take LPs on a journey to give them comfort that you have the ability to outperform, using your operating resource, as it comes to the funds you are currently raising and deploying. Here is a small selection of questions that we explore with the GPs we work with:

If you’d like to know more about how we can help optimise any aspect of your GP’s strategy, stakeholder engagement or operations, don’t hesitate to reach out to us!

AccelNorth Partners is an advisor specialising in the private markets industry. Whether you’re a GP or an LP, reach out to us to discuss your strategic, operational, diligence, fundraising and IR challenges. Email us at info@accelnorthpartners.com. And follow us on Medium.